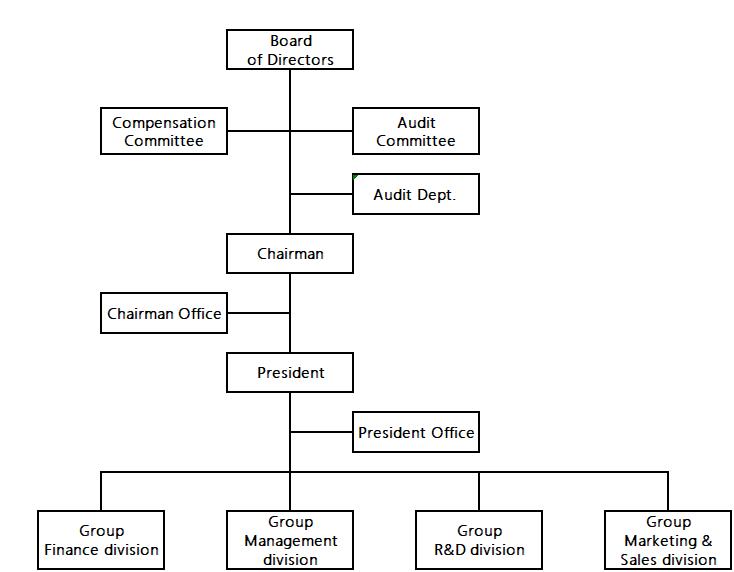

1. Organization of audit unit and auditors

The Audit Office of the Company is subordinate to the board of directors. In addition to reporting audit business to the Audit Committee on a regular basis, the audit director also attends the report of the board of directors.The audit office shall set up an internal audit supervisor and internal auditors, whose relevant experience shall meet the requirements of legal qualification. The appointment and removal of the audit supervisor shall be approved by the board of directors, and the appointment, removal, evaluation, salary and remuneration of the internal auditors shall be signed by the Audit Supervisor and approved by the chairman of the board of directors.

2.Scope of internal audit

(1)The scope of internal audit includes all the business that each unit of the Company is responsible for, and all the businesses of subsidiaries without audit unit.

(2)The scope of the Company's internal audit shall at least include the following items: A. To check the internal control system, so as to measure the effectiveness and compliance of the current policies and procedures and their impact on various operating activities. B. Determine the audit project, time, procedure and method.

(3)The scope of internal audit should cover all operation activities, and mainly focus on transaction cycle types, which can be divided into the following control operations: Sales and collection, procurement and payment, production, payroll, financing, real estate, plant and equipment, investment, R & D and other cycle operations. In addition, in order to strengthen the management of internal control operations, the Company increases the following control operations: endorsement and guarantee, management of transactions between capital loans and others and related parties.

3.Responsibilities of audit unit

The role of the audit office is to assist the board of directors and senior management to independently and objectively assess the completeness, effectiveness and implementation of the Company's internal control system, and to provide timely improvement suggestions, so as to reasonably ensure the continuous and effective implementation of the internal control system. At the same time, it provides relevant investigation, evaluation or consultation services as appointed by the board of directors and senior management to assist the board of directors and senior management to fulfill their corporate governance responsibilities.

4.Operation of internal audit

(1)The audit office shall draw up an annual audit plan based on the results of risk assessment. The audit plan shall be submitted to the board of directors for examination and approval, and shall be implemented accordingly. The same shall apply to the amendment.

(2)The annual audit plan shall include but not be limited to the audit items required by the competent authority. The audit office shall attach the working paper and relevant materials to the audit report for the deficiencies and abnormalities of the internal control system found in the audit items, and continuously track them to ensure that the relevant units have taken appropriate improvement measures.

(3)The director of audit regularly reports the lack of internal control to the audit committee and the board of directors and tracks the improvement. If the auditor finds any material violation or the Company is in danger of material damage, he shall immediately make a report to the audit committee.

(4)The lack of internal control and improvement of abnormal matters found by the audit office shall be the main basis for the board of directors to evaluate the effectiveness of the overall internal control system and issue a statement on the internal control system.

(5)The audit office shall, in accordance with the format prescribed by the competent authority, make regular and irregular internal control related declaration.

Regular internal control declaration

(1)Before the end of each year, report the audit plan for the next year.

(2)Before the end of January every year, report the list of auditors and the status of their further study.

(3)Before the end of February of each year, report the implementation of the annual audit plan of the previous year.

(4)Before the end of March of each year, report the internal control system statement of the previous year.

(5)Before the end of May of each year, report the improvement of internal control system deficiencies and abnormal events of the previous year.

Irregular internal control declaration

(1)When a CPA is invited to conduct a special audit of internal control, it shall input the report into the public information Observatory within 2 days from the date of obtaining the special audit report.

+886-7-5528802

+886-7-5528802